In recent times, there's a common jest about everything getting more expensive except one's salary, given the economic downturn and rising prices, yet salaries remain unchanged. In such times, smart investments to create multiple income streams become essential. However, diversifying income also brings along various taxes, which can freeze your bank account. So, how should we deal with these taxes? Hyundai Securities has gathered experts from various fields to write a guidebook on saving taxes, covering income, taxes, and methods to reduce taxes in Korea.

During Korea's economic boom, a single income family could live just fine. However, in today's stable economy, such lifestyle is challenging for everybody. Thus, many are striving to increase their income through financial earnings, stock investments, and family inheritances and gifts. Here, experts from Hyundai Securities highlight these three key ideas in their tax-saving guidebook as well.

Financial income refers to interest and dividends received from various financial products (e.g., savings accounts, CMA, stocks, ETFs, pension savings). It's the foundation of wealth management and diversification. Naturally, taxes are levied on financial income, and using specific financial products can help reduce these taxes. Notably, the type of investment and resulting profit or loss can affect the amount of tax owed. With increasing cases of inheritance and gifting within families, it's also essential to know how to save on inheritance and gift taxes.

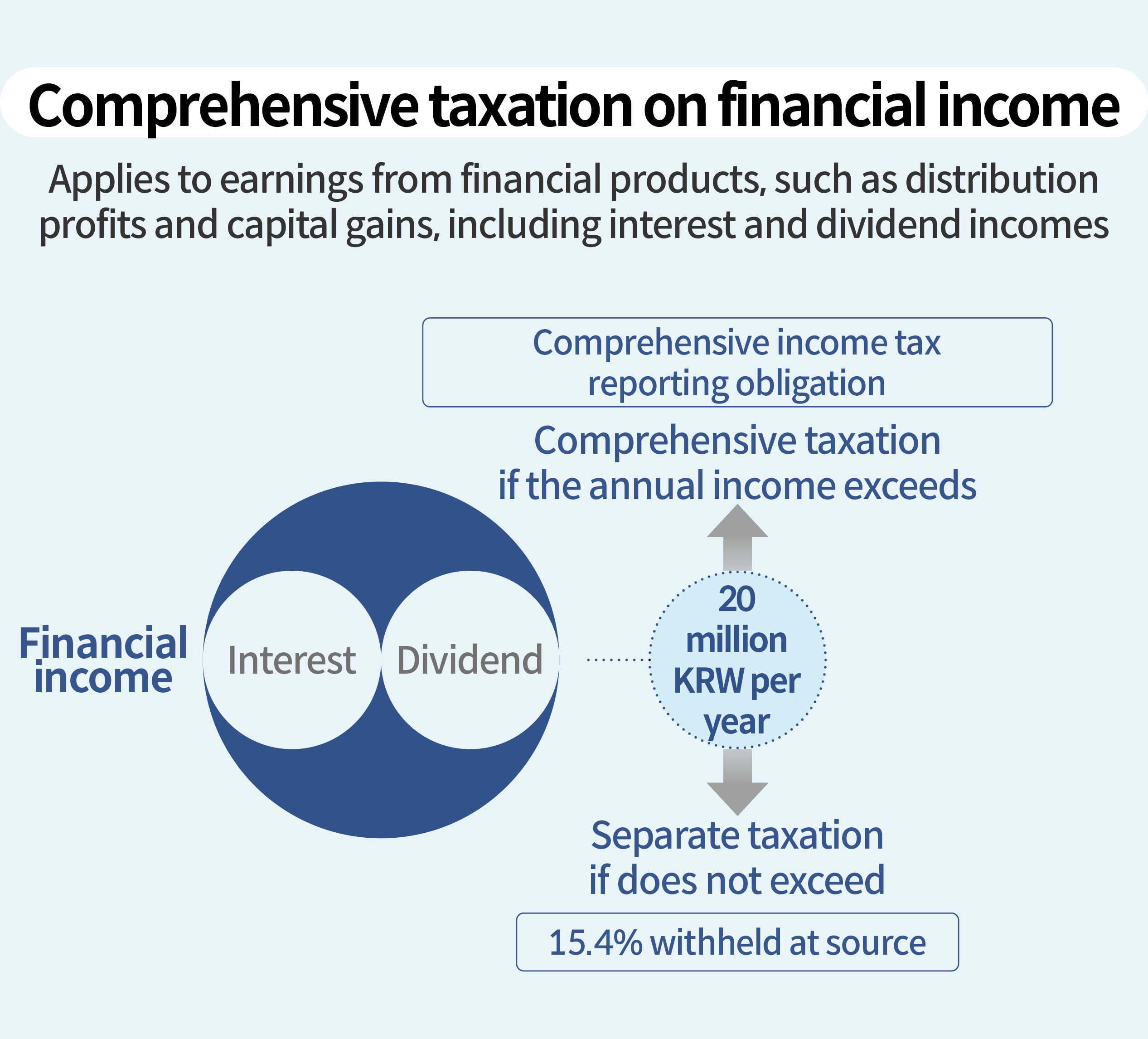

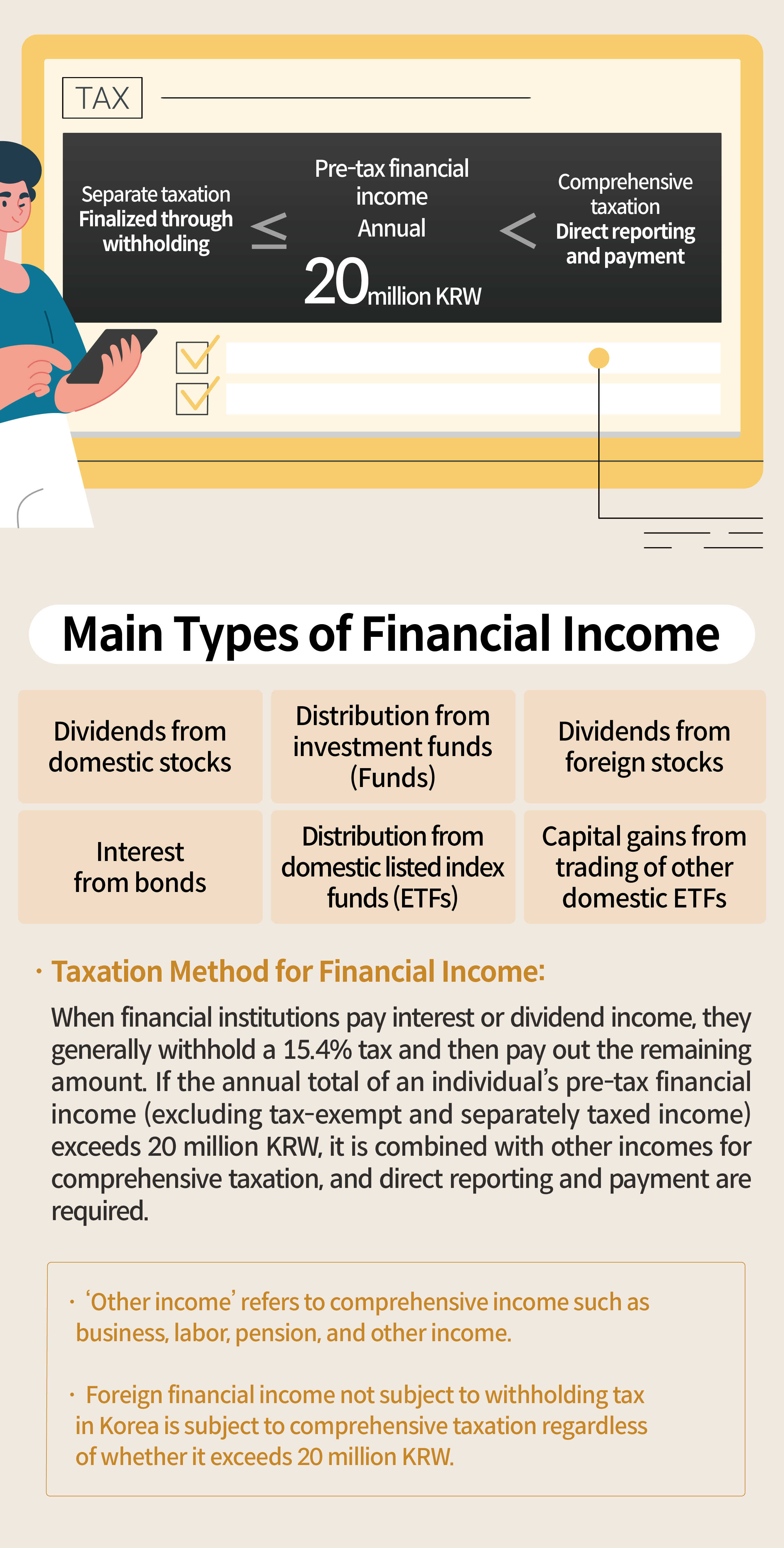

Hyundai Securities' first tax-saving keyword is 'comprehensive taxation on financial income.' This refers to income generated from investments in products offered by financial institutions, like savings accounts, CMA, bonds, stock dividends, and fund or ETF distributions. Financial institutions withhold a 15.4% tax on interest and dividend income before paying the investor. If the total financial income for the year exceeds 20 million KRW before tax, it's combined with other income types (e.g., employment, pension, business income) for comprehensive taxation. The basic tax rate for this is progressive, ranging from 6.6% to 49.5%.

Another aspect to consider in comprehensive taxation is health insurance premiums. For employed income earners, health insurance premiums consist of a salary-based insurance premium (4% of salary) and an income-based premium ( [non-salary income - 20 million KRW] × 8%). If non-salary income, such as interest, dividends, pensions, business, and other income, exceeds 20 million KRW, the monthly health insurance premium increases accordingly. For example, if you have an annual financial income of 24 million KRW, then the income beyond the salary (24 million KRW) would be reduced by 20 million KRW, leaving 4 million KRW subject to an 8% rate for the income-based health insurance premium. Dividing this over 12 months, you would need to pay an additional health insurance premium of about 27,000 KRW each month.

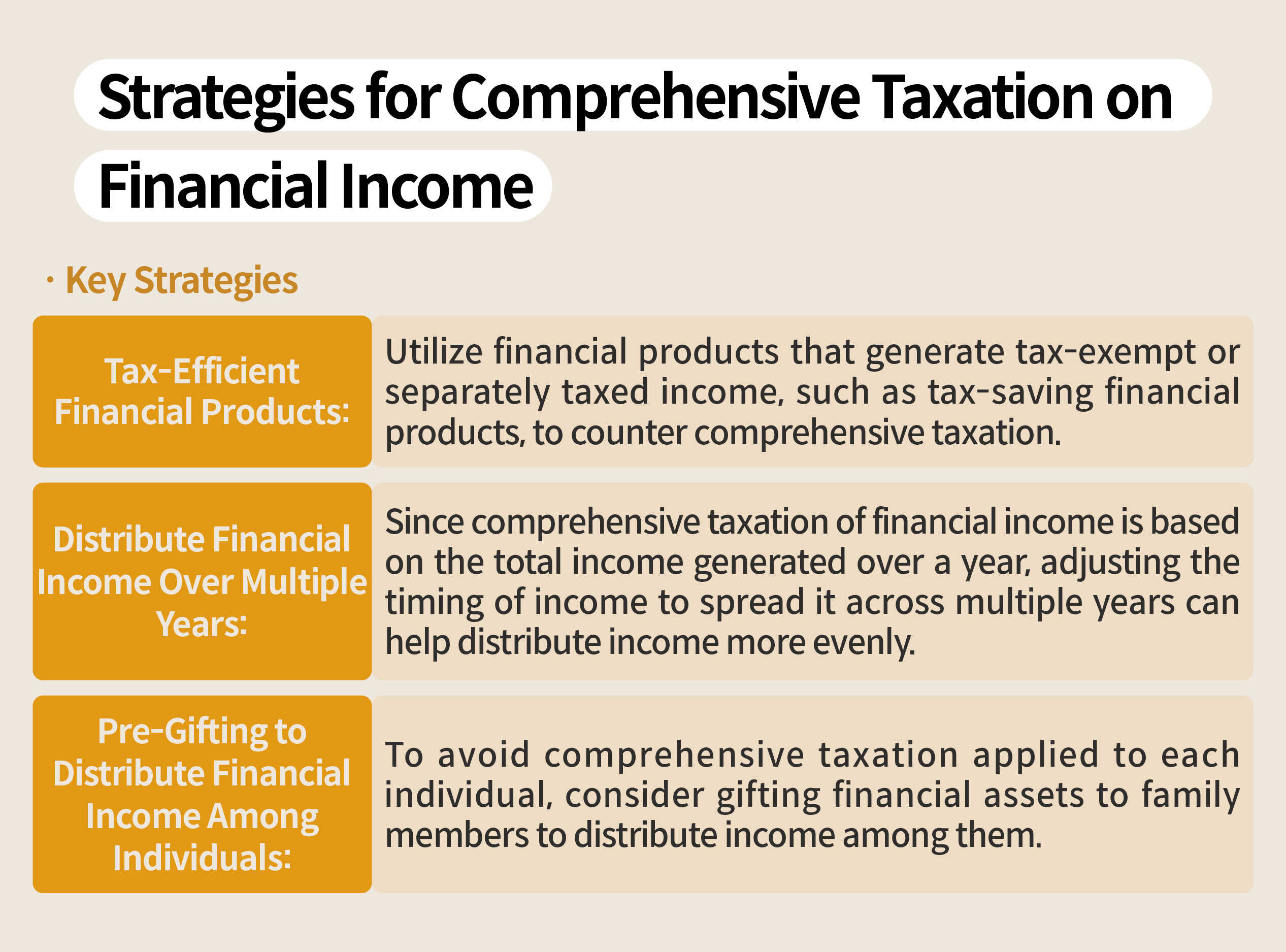

Investors who have diversified their income across various sectors might feel burdened by the accompanying taxes. So, what can be done to alleviate the comprehensive taxation burden? Hyundai Securities recommends three strategies: The first is to use tax-exempt and separately taxed financial products. The financial income generated from these products does not count towards the comprehensive taxation threshold of 20 million KRW. While it might not be feasible to invest entirely in these products, actively utilizing tax-exempt and separately taxed financial products and diversifying investments to stay below the comprehensive taxation threshold is advisable. Such financial products include tax-exempt savings accounts, long-term savings insurance, pension savings, IRP, and ISA.

The second strategy involves spreading out the timing of income. Comprehensive taxation of financial income aggregates all financial income generated from January 1 to December 31 each year. Thus, to ensure the annual financial income does not exceed 20 million KRW, it is wise to adjust the subs-cription period of products or use cancellation and redemption to spread out income over time.

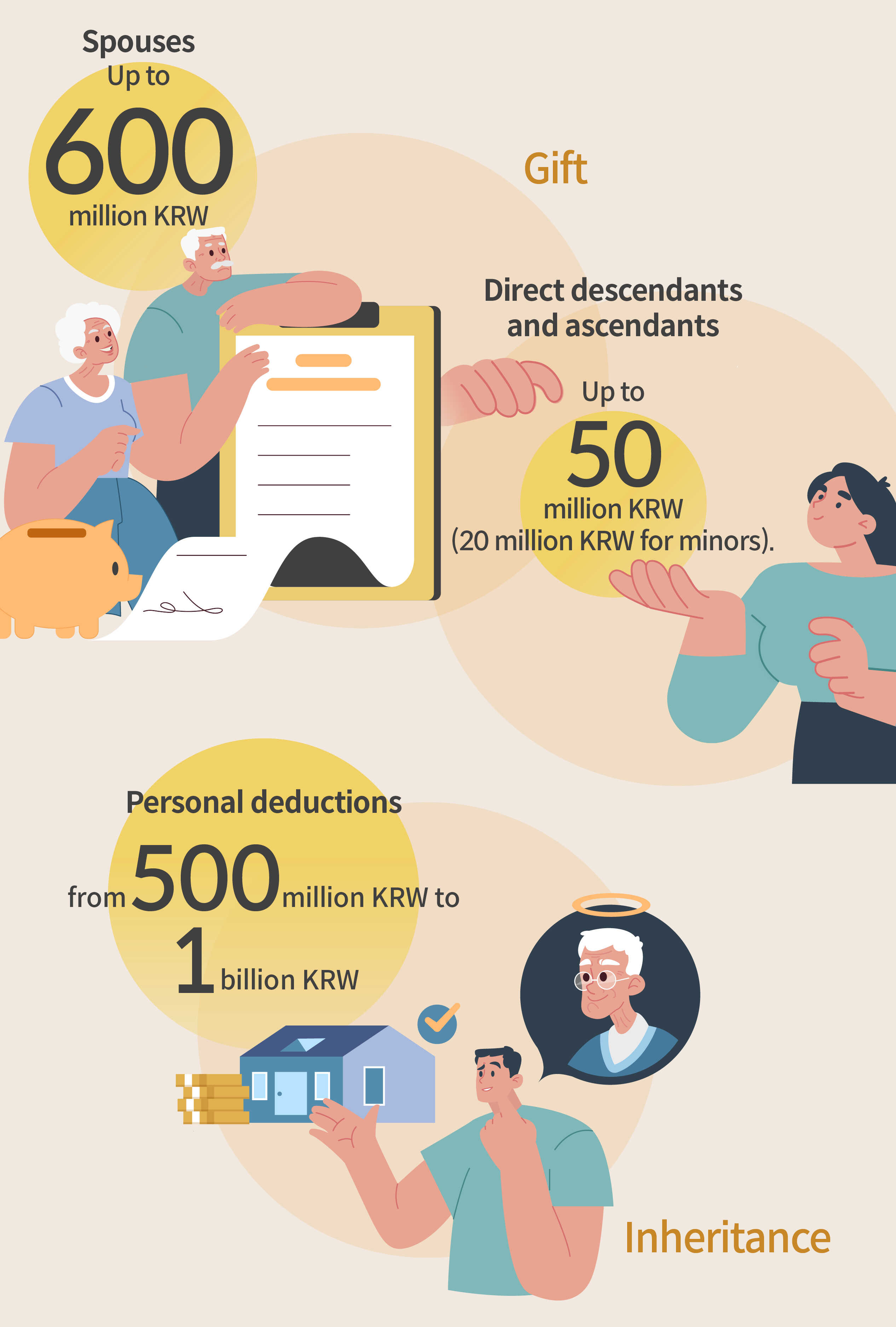

Lastly, preemptive gifting to distribute financial income can reduce income tax. Gifting financial income to family members can disperse the income received by each individual, maintaining the existing income while avoiding comprehensive taxation. Additionally, gift tax is progressively taxed by aggregating all gifts given over 10 years. If the gift tax exemption limit is observed, gift tax may not be necessary. The exemption limit varies depending on the relationship between the donor and the recipient: 600 million KRW for spouses, 50 million KRW for direct ascendants (20 million KRW when gifting to minors), 50 million KRW for direct descendants, and 10 million KRW for other relatives.

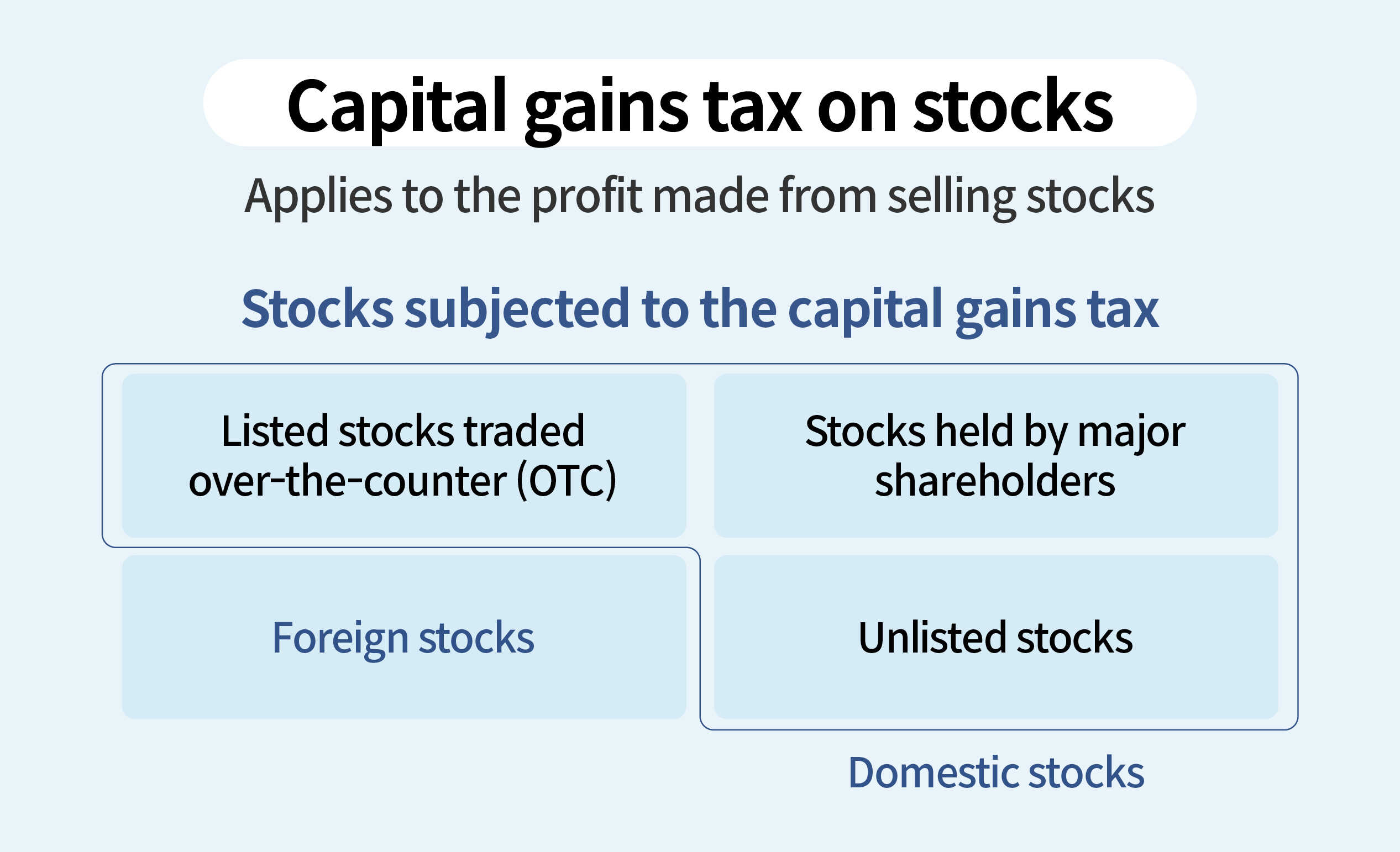

Among various investment incomes, stock investments incur taxes during trading. Capital gains tax is applied to profits made from buying and selling stocks. While small shareholders selling domestic listed stocks on the market are exempt, large shareholders, off-market transactions, unlisted stocks, and foreign stocks are taxed. The tax amount for capital gains tax is calculated by subtracting a basic exemption of 2.5 million won from the taxable amount (sale price minus acquisition cost, securities transaction tax, fees, etc.) and applying a tax rate. For large shareholders, the tax rate varies depending on the taxable standard, necessitating consideration for tax-saving strategies.

To mitigate capital gains tax as a major shareholder, classified based on shareholding ratio or market capitalization, three main strategies are suggested. First, if the valuation of stocks held on the last trading day, December 30 (as of 2024), is below 5 billion KRW, one isn't considered a major shareholder, thus exempt from capital gains tax. Second, gifting stocks among family members can be a tax-saving strategy since it can lower the total value of stocks held by an individual below the 5 billion KRW threshold. Lastly, increasing the acquisition cost through repurchasing stocks can reduce capital gains tax, even for major shareholders, by decreasing the net profit from sales.

For foreign stocks, which are also subject to capital gains tax, a 22% tax rate applies to the profit made from sales. The tax for foreign stocks must be declared and paid once a year in May, following the year the stocks were sold. To save on taxes for foreign stock sales, it's advisable to check the settlement dates for each stock and spread the sales over different years. Since profits up to 2.5 million KRW are exempt, it's beneficial to sell foreign stocks within this limit, postponing the sale of any amount over this threshold to the next year. Additionally, strategies like offsetting with domestic stock sales or gifting among family members are also recommended for tax savings.

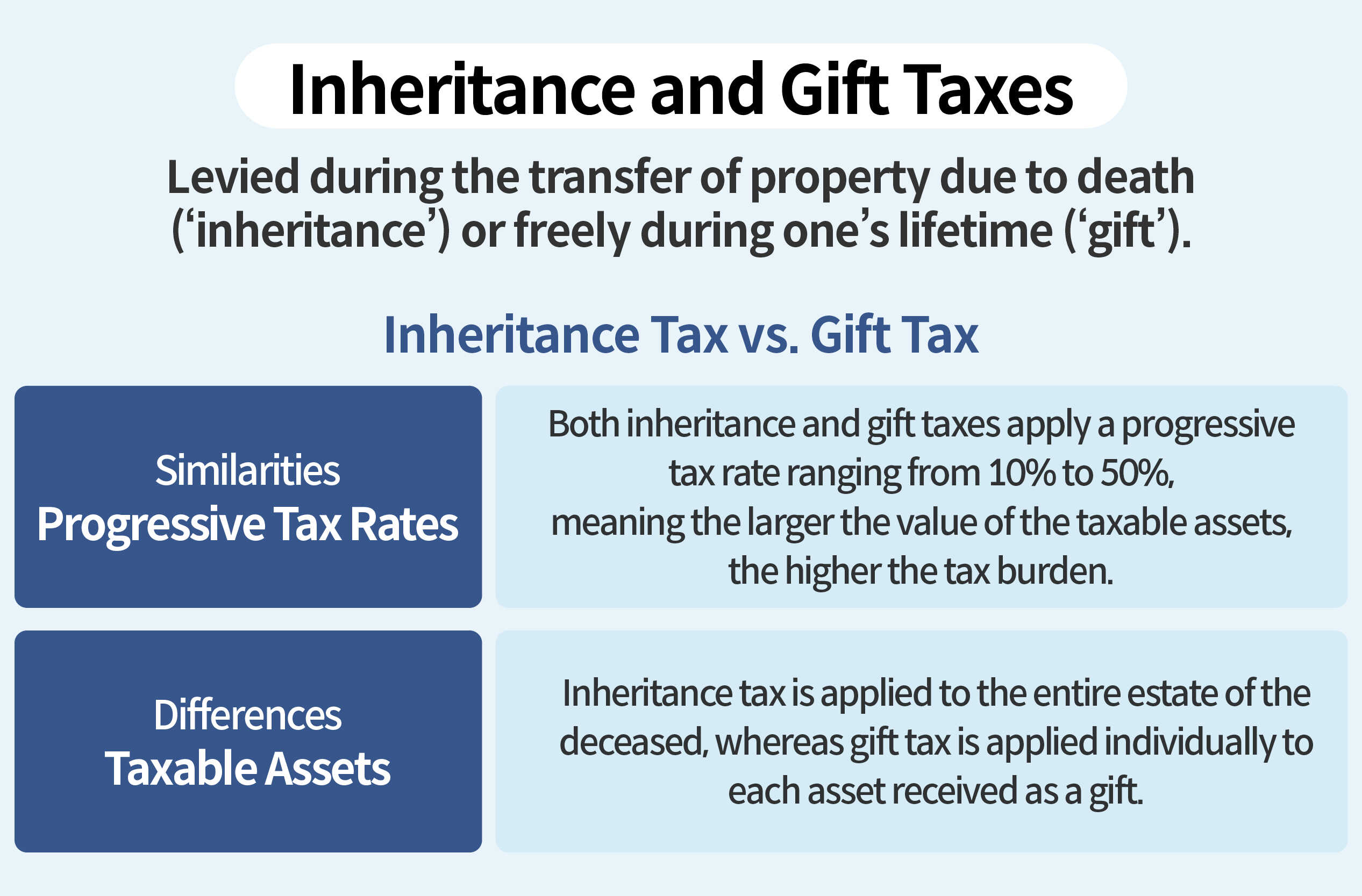

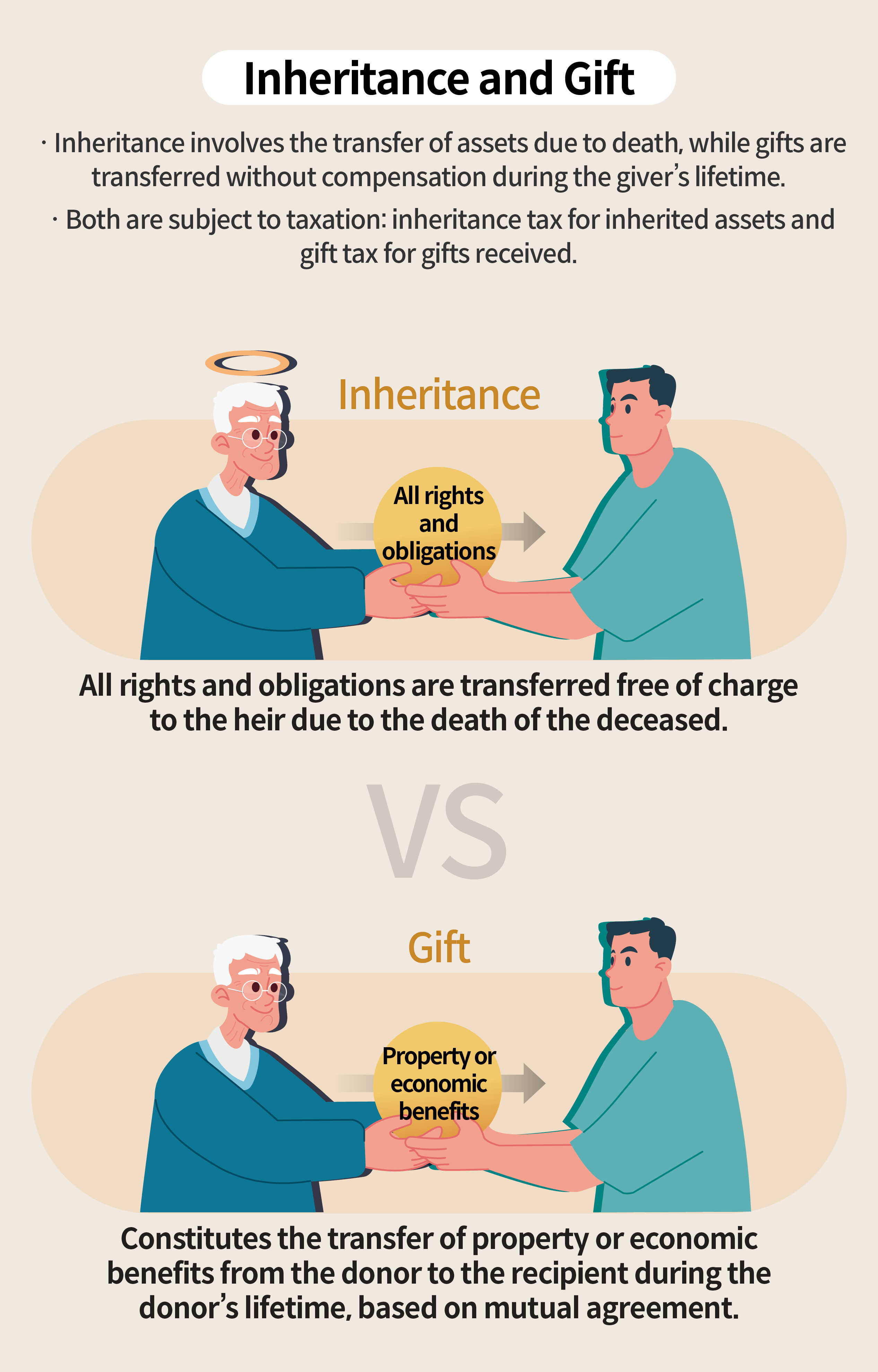

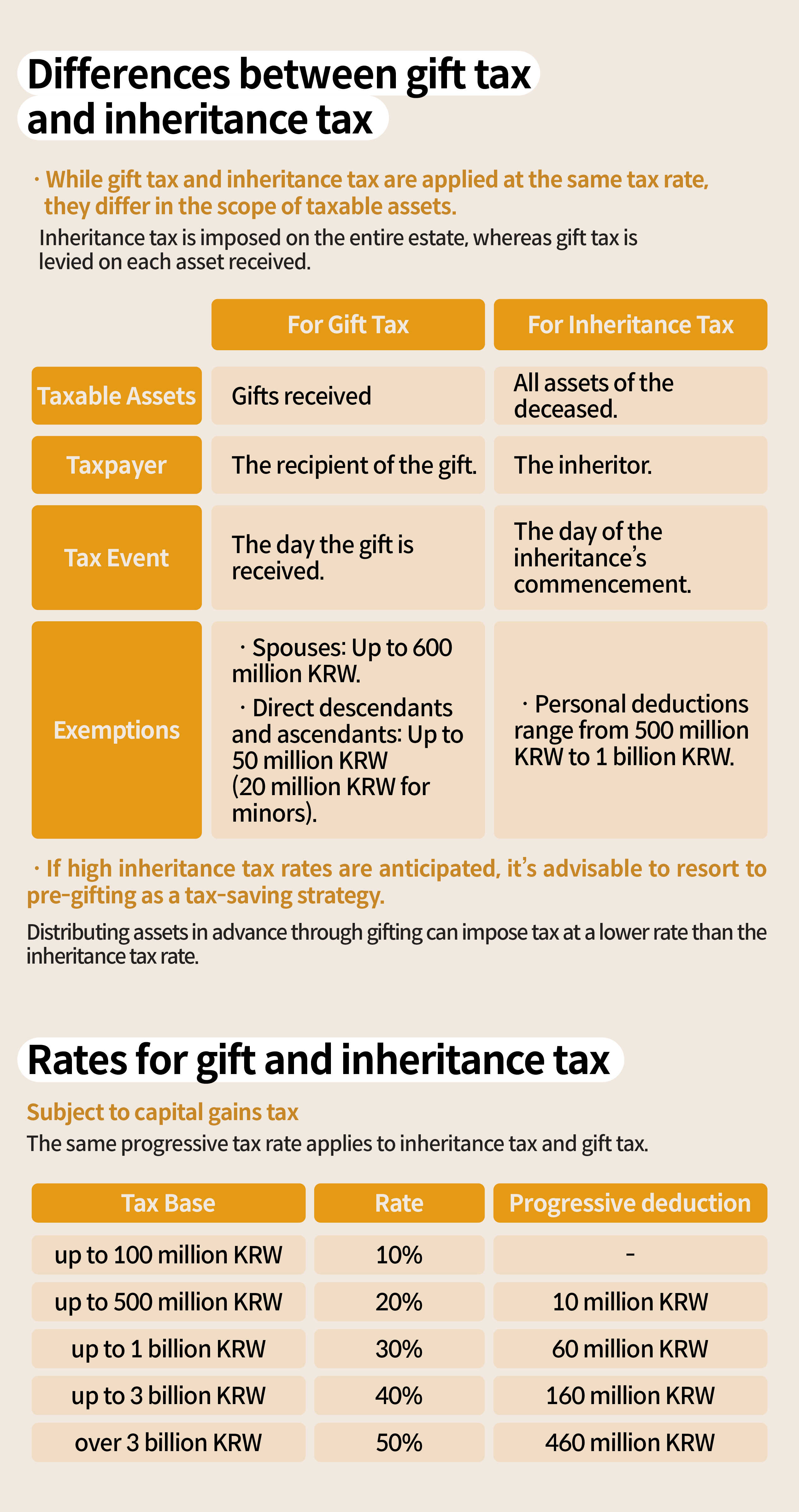

While inheritance and gifting were once considered concerns of the wealthy, it's now common in the middle class for parents to pass down apartments, cars, and other assets to their children, raising interest in the related taxes. Both inheritance and gifting involve the transfer of wealth within a family, but there are key differences. Inheritance is the transfer of rights and obligations upon the death of the inheritor, while gifting is the transfer of property or economic benefits based on mutual consent without compensation. Despite their similarities, the tax standards for inheritance and gifting differ.

Inheritance tax applies to all the deceased's assets, while gift tax is based solely on gifted property. The tax obligation falls on the recipient in both cases. The timing for taxation is based on the date of inheritance or the day the gift is received. Inheritance tax allows for personal deductions ranging from 500 million to 1 billion KRW, whereas gift tax varies depending on the relationship between the giver and the recipient (600 million KRW for spouses, 50 million KRW for direct descendants or ancestors, with specific amounts for minors and other relatives). While the tax rates are the same, inheritance tax is levied on the total estate, and gift tax is assessed on each gifted property. To save on taxes, spreading out the estate through gifting before inheritance can be beneficial.

Gift tax is consolidated over a ten-year period for property received from the same person. During this time, a certain amount can be deducted based on the relationship between the giver and the receiver. The exemption limits are 600 million KRW for spouses, 50 million KRW for direct ancestors (20 million KRW if the recipient is a minor), 50 million KRW for direct descendants, and 10 million KRW for other relatives. To reduce gift tax, it's advisable to check the relationship with the recipient and gift within these exemption limits. Since the tax assessment period is based on ten years, gifting within the exemption limits every ten years can prevent gift tax. When grandparents gift to their grandchildren, a 30% tax surcharge is incurred. However, when considering the overall family finances, paying the 30% surcharge instead of paying gift tax twice can actually be beneficial. Strategically spreading and gifting assets in advance, with a long-term perspective, is the best strategy to reduce taxes from inheritance and gifting, thus preserving family wealth.

Although there's a negative perception that taxes unjustly take away the fruits of one's labor, taxes are vital for the functioning of the state and the market economy. As citizens, it's obligatory to fulfill tax duties. However, utilizing legal tax-saving strategies can aid in personal financial management. The tax-saving guidebook compiled by Hyundai Securities experts aims to assist clients in fulfilling their duties while protecting their assets.